Personal Loan

Personal Loan Check Eligibility

Check Eligibility Salaried Personal Loan

Salaried Personal Loan EMI Calculator

EMI Calculator Account Aggregator

Account Aggregator

Deals starting @99

Deals starting @99 Min. 50% off

Min. 50% off

Bajaj Pay

Bajaj Pay Wallet to Bank

Wallet to Bank

Easy EMI Loan

Easy EMI Loan Savings Offer

Savings Offer Smartphones

Smartphones Led TVs

Led TVs Washing Machines

Washing Machines Laptops

Laptops Refrigerators

Refrigerators Air Conditioner

Air Conditioner Air Coolers

Air Coolers

Loan Against Shares

Loan Against Shares Loan Against Mutual Funds

Loan Against Mutual Funds Loan Against Insurance Policy

Loan Against Insurance Policy ESOP Financing

ESOP Financing Easy EMI Loan

Easy EMI Loan Buy a Used Car

Buy a Used Car New Tractor Loan

New Tractor Loan Two-wheeler Loan

Two-wheeler Loan Loan for Lawyer

Loan for Lawyer Industrial Equipment Finance

Industrial Equipment Finance Industrial Equipment Balance Transfer

Industrial Equipment Balance Transfer Industrial Equipment Refinance

Industrial Equipment Refinance Personal Loan Branch Locator

Personal Loan Branch Locator Used Tractor Loan

Used Tractor Loan Loan Against Tractor

Loan Against Tractor Tractor Loan Balance Transfer

Tractor Loan Balance Transfer Flexi

Flexi View All

View All

Two-wheeler Loan

Two-wheeler Loan Bike

Bike Commuter Bike

Commuter Bike Sports Bike

Sports Bike Tourer Bike

Tourer Bike Cruiser Bike

Cruiser Bike Adventure Bike

Adventure Bike Scooter

Scooter Electric Vehicle

Electric Vehicle Best Sellers

Best Sellers Popular Brands

Popular Brands

Trading Account

Trading Account Open Demat Account

Open Demat Account Margin Trading Financing

Margin Trading Financing Share Market

Share Market Invest in IPO

Invest in IPO All stocks

All stocks Top gainers

Top gainers Top losers

Top losers 52 week high

52 week high 52 week low

52 week low Loan against shares

Loan against shares

Home Loan

Home Loan Transfer your existing Home loan

Transfer your existing Home loan Loan against Property

Loan against Property Home Loan for Salaried

Home Loan for Salaried Home loan for self employed

Home loan for self employed Loan Against Property Balance Transfer

Loan Against Property Balance Transfer Home Loan EMI Calculator

Home Loan EMI Calculator Home Loan eligibility calculator

Home Loan eligibility calculator Home Loan balance transfer

Home Loan balance transfer View All

View All

Term Life Insurance

Term Life Insurance ULIP Plan

ULIP Plan Savings Plan

Savings Plan Family Insurance

Family Insurance Senior Citizen Health Insurance

Senior Citizen Health Insurance Critical Illness Insurance

Critical Illness Insurance Child Health Insurance

Child Health Insurance Pregnancy and Maternity Health Insurance

Pregnancy and Maternity Health Insurance Individual Health Insurance

Individual Health Insurance Low Income Health Insurance

Low Income Health Insurance Student Health Insurance

Student Health Insurance Group Health Insurance

Group Health Insurance Retirement Plans

Retirement Plans Child Plans

Child Plans Investment Plans

Investment Plans

Business Loan

Business Loan Secured Business Loan

Secured Business Loan Loan against property

Loan against property Loans against property balance transfer

Loans against property balance transfer Loan against shares

Loan against shares Home Loan

Home Loan Loans against mutual funds

Loans against mutual funds Loan against bonds

Loan against bonds Loan against insurance policy

Loan against insurance policy

Apply for Gold Loan

Apply for Gold Loan Transfer your Gold Loan with Us

Transfer your Gold Loan with Us Gold Loan Branch Locator

Gold Loan Branch Locator

ULIP Plan

ULIP Plan Savings Plan

Savings Plan Retirement Plans

Retirement Plans Child Plans

Child Plans Free Demat Account

Free Demat Account Invest in Stocks

Invest in Stocks Invest in IPO

Invest in IPO Margin Trading Facility

Margin Trading Facility Fixed Deposit Branch Locator

Fixed Deposit Branch Locator

New Car Loan

New Car Loan Used Car Loan

Used Car Loan Loan Against Car

Loan Against Car Car Loan Balance Transfer and Top-up

Car Loan Balance Transfer and Top-up My Garage

My Garage

Get Bajaj Prime

Get Bajaj Prime

Mobiles on EMI

Mobiles on EMI Electronics on EMI Offer

Electronics on EMI Offer  Iphone on EMI

Iphone on EMI LED TV on EMI

LED TV on EMI Refrigerator on EMI

Refrigerator on EMI Laptop on EMI

Laptop on EMI Kitchen appliances on EMI

Kitchen appliances on EMI Washing machines

Washing machines

Personal Loan EMI Calculator

Personal Loan EMI Calculator Personal Loan Eligibility Calculator

Personal Loan Eligibility Calculator Home Loan EMI Calculator

Home Loan EMI Calculator Home Loan Eligibility Calculator

Home Loan Eligibility Calculator Good & Service Tax (GST) Calculator

Good & Service Tax (GST) Calculator Flexi Day Wise Interest Calculator

Flexi Day Wise Interest Calculator Flexi Transaction Calculator

Flexi Transaction Calculator Secured Business Loan Eligibility Calculator

Secured Business Loan Eligibility Calculator Fixed Deposits Interest Calculator

Fixed Deposits Interest Calculator Two wheeler Loan EMI Calculator

Two wheeler Loan EMI Calculator New Car Loan EMI Calculator

New Car Loan EMI Calculator Used Car Loan EMI Calculator

Used Car Loan EMI Calculator All Calculator

All Calculator Used Tractor Loan EMI Calculator

Used Tractor Loan EMI Calculator

Hot Deals

Hot Deals Clearance Sale

Clearance Sale Kitchen Appliances

Kitchen Appliances Tyres

Tyres Camera & Accessories

Camera & Accessories Mattresses

Mattresses Furniture

Furniture Watches

Watches Music & Audio

Music & Audio Cycles

Cycles Mixer & Grinder

Mixer & Grinder Luggage & Travel

Luggage & Travel Fitness Equipment

Fitness Equipment Fans

Fans

Personal Loan for Doctors

Personal Loan for Doctors Business loan for Doctors

Business loan for Doctors Home Loan

Home Loan Secured Business Loan

Secured Business Loan Loan against property

Loan against property Secured Business Loan Balance Transfer

Secured Business Loan Balance Transfer Loan against share

Loan against share Gold Loan

Gold Loan Medical Equipment Finance

Medical Equipment Finance

Smart Hub

Smart Hub ITR Service

ITR Service Digi Sarkar

Digi Sarkar

Savings Offer

Savings Offer Easy EMI

Easy EMI Offer World

Offer World 1 EMI OFF

1 EMI OFF New Launches

New Launches Zero Down Payment

Zero Down Payment Clearance Sale

Clearance Sale Bajaj Mall Sale

Bajaj Mall Sale

Mobiles under ₹20,000

Mobiles under ₹20,000 Mobiles under ₹25,000

Mobiles under ₹25,000 Mobiles under ₹30,000

Mobiles under ₹30,000 Mobiles under ₹35,000

Mobiles under ₹35,000 Mobiles under ₹40,000

Mobiles under ₹40,000 Mobiles under ₹50,000

Mobiles under ₹50,000

Articles

Articles

Overdue Payments

Overdue Payments Other Payments

Other Payments

Document Center

Document Center Bank details & Documents

Bank details & Documents Tax Invoice Certificate

Tax Invoice Certificate

Do Not Call Service

Do Not Call Service

Hamara Mall Orders

Hamara Mall Orders Your Orders

Your Orders

Explore Bajaj Prime

Explore Bajaj Prime Explore Rewards

Explore Rewards Buy Deals & Gift cards

Buy Deals & Gift cards

Fixed Deposit (IFA) Partner

Fixed Deposit (IFA) Partner Loan (DSA) Partner

Loan (DSA) Partner Debt Management Partner

Debt Management Partner EMI Network Partner

EMI Network Partner Became a Merchant

Became a Merchant Partner Sign-in

Partner Sign-in

Trade directly with your Demat A/c

Trade directly with your Demat A/c ITR

ITR My Garage

My Garage

Live Videos - Beta

Live Videos - Beta

Savings Offer

Savings Offer Smartphones

Smartphones LED TVs

LED TVs Washing Machines

Washing Machines Laptops

Laptops Refrigerators

Refrigerators Air Conditioners

Air Conditioners Air Coolers

Air Coolers Water Purifiers

Water Purifiers Tablets

Tablets Kitchen Appliances

Kitchen Appliances Mattresses

Mattresses Furniture

Furniture Music and Audio

Music and Audio Cameras & Accessories

Cameras & Accessories Cycle

Cycle Watches

Watches Tyres

Tyres Luggage & Travel

Luggage & Travel Fitness Equipment

Fitness Equipment Tractor

Tractor Easy EMI Loan

Easy EMI Loan

vivo Mobiles

vivo Mobiles OPPO Mobiles

OPPO Mobiles Xiaomi Mobiles

Xiaomi Mobiles Sony LED TVs

Sony LED TVs Samsung LED TVs

Samsung LED TVs LG LED TVs

LG LED TVs Haier LED TVs

Haier LED TVs Godrej Refrigerators

Godrej Refrigerators Voltas Washing Machines

Voltas Washing Machines

New Tractor Loan

New Tractor Loan Used Tractor Loan

Used Tractor Loan Loan Against Tractor

Loan Against Tractor Tractor Loan Balance Transfer

Tractor Loan Balance Transfer

New Car Loan

New Car Loan New Cars Under ₹10 Lakh

New Cars Under ₹10 Lakh New Cars – ₹10–₹15 Lakh

New Cars – ₹10–₹15 Lakh New Cars – ₹15–₹20 Lakh

New Cars – ₹15–₹20 Lakh New Cars – ₹20–₹25 Lakh

New Cars – ₹20–₹25 Lakh New Car Brands

New Car Brands Petrol – New Cars

Petrol – New Cars Diesel – New Cars

Diesel – New Cars Electric – New Cars

Electric – New Cars CNG – New Cars

CNG – New Cars Hybrid – New Cars

Hybrid – New Cars

Select the loan amount you want

Bestsellers for self-employed individuals

Trending loans

Frequently asked questions

A home loan is a credit borrowed from a financial institution to buy a home. The home loan is given at an interest rate depending on your profile. While taking the loan, you choose a repayment period to pay back the amount (principal) and interest in equated monthly instalments (EMIs). You can either choose a fixed interest rate or a floating interest rate.

You can easily get a home loan up to Rs. 15 Crore* from Bajaj Finserv if you meet our eligibility criteria. The sanctioned loan amount depends upon essential factors like your age, income profile, CIBIL Score, and among other criteria.

Salaried professionals applying for a fresh home loan with Bajaj Finserv, must have the listed documents:

- KYC documents (identity and address proof)

- Proof of income (salary slips)

- Account statements for the last 6 months

Self-employed individuals applying for a fresh home loan from Bajaj Finserv, must have the listed documents:

- KYC documents (identity and address proof)

- Proof of income (P&L statement)

- Proof of business

- Last 6 months' account statements, etc.

Once you have submitted all the essential documents, the loan amount will be approved within 48 Hours*. In some cases, it can get sanctioned even earlier.

* Terms and conditions apply

You can get tax benefits on home loan. Home loan tax benefits include deduction of Rs. 1.5 lakh on the principal amount under Section 80C. Additionally, Section 24B allows tax deduction of Rs. 2 lakh on the interest repayment. You can also claim tax deductions for registration fees and stamp duty charges under Section 80C.

You start paying your home loan EMI when the disbursement cheque is created. Once you receive the loan amount, you begin paying EMIs as per the EMI cycle. This means if your chosen date for EMI repayment is the 5th of a month and you receive the loan on the 28th of the month, then for the first month you pay EMI calculated from the day your house loan was sanctioned to your first EMI date. Next month onwards, you pay regular EMIs on the designated day.

Yes, if you want to get a bigger loan, you can take opt for a joint home loan. Family members, such as spouses, parents, siblings, and offspring, can be co-applicants for a joint house loan.

The processing fee is among the fees that you'll have to pay on a home loan. A home loan processing fee is a one-time fee charged by the lender once your housing loan application has been accepted. While some lenders charge a processing fee for home loans, others do not.

A home loan is secured in nature, i.e., the loan amount is sanctioned against a collateral, which is the property in question.

The loan amount is sanctioned at a predetermined interest for an agreed-to period, also known as the ‘tenure.’ The borrower repays the loan with interest through a home loan EMI, payable every month. The property ownership remains with the lender till the home loan repayment is complete, including interest.

No. As per RBI guidelines, no lender is permitted to offer 100% home financing. You need to make a down payment amounting to 10-20% of the property’s purchase price. Typically, you can obtain up to 80% housing loan financing for your property.

Both types of home loans have their pros and cons. With a fixed-rate home loan, the interest rate remains constant through the tenor, which allows you to forecast EMIs. Pick it when home loan interest rates are low and when you want fixed EMIs.

With floating-rate home loans, the interest rate alters basis economic changes and RBI policy decisions. Choose this variant when you expect rates to reduce in the time to come. Additionally, the RBI mandates that you do not need to pay any prepayment or foreclosure charges if you’re an individual borrowing a floating rate home loan.

Basis the different requirements for home finance and varied customer profiles, the types of home loans available in India are:

- Home construction loan

- Home loan balance transfer

- Top-up loan

- Joint home loan

- Loans under the Pradhan Mantri Awas Yojana scheme

Home loan for:

- Women

- Government Employees

- Advocates

- Bank Employees

- Private Employees

Availing of a house loan requires an individual to meet the eligibility criteria that ensure a borrower’s capacity to repay. The factors that affect eligibility are:

- A person’s credit score

- Monthly income

- Current financial obligations and debt

- Employment status

- Age of the applicant

- Property to be purchased

Yes, you can switch from a floating rate of interest to a fixed rate during the repayment tenor of your housing loan. You need to pay a nominal amount as a conversion fee to your lender for switching.

Opting for a housing loan is a smart financial decision for the following reasons:

- It brings additional financing to fund your housing dreams without affecting your savings

- You can choose from several housing loan options as per your requirements

- The interest rates are affordable and make loan repayment more convenient

- Long tenor allows for repayment towards the loan in easy EMIs

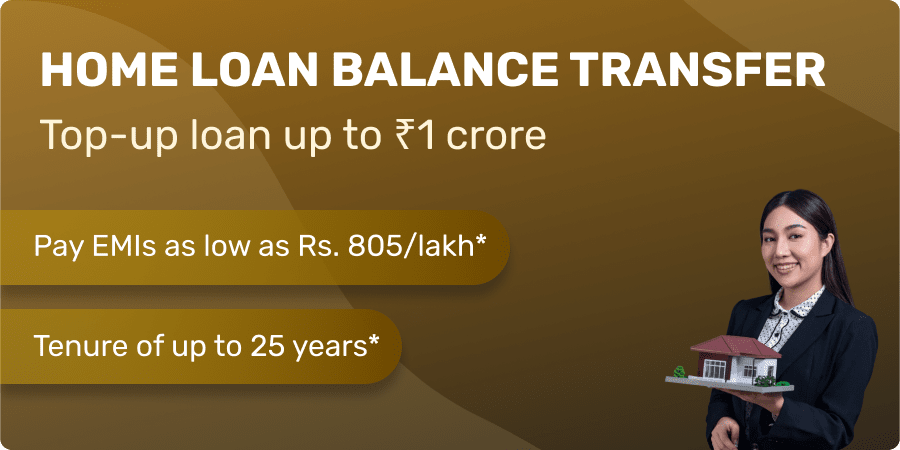

No, availing two housing loans at a time for the same property is restricted as per the CERSAI. However, individuals can opt for a house loan balance transfer to refinance their existing housing credit at a lower rate of interest. The facility comes with the top-up loan facility - an additional loan over and above the existing loan amount. Avail the funds to meet diverse financial necessities with ease.

Proceed with the following steps to avail a home loan with ease.

- Check your credit reports and rectify errors, if any

- Estimate EMIs with a home loan calculator and decide on the loan amount as per repayment capacity

- Keep all the necessary documents handy

- Compare the available offers for the best housing loan option

- Ensure to meet all eligibility before applying

The repayment period for loans begins immediately after the lender has disbursed the entire housing loan amount. However, in cases of partial disbursal, the interest accrued on such a disbursed amount is required to be paid as pre-EMI. Full EMI payment including the principal and interest amount starts after full disbursal of the loan.

No, it is not mandatory that you take home loan insurance along with your loan. However, you may consider getting insurance to take care of any liability at a marginal increase in your EMIs.

You can check the status of your housing loan application online by entering your home loan application number/ ID, as well as your mobile number/ contact information.

You can also contact your home loan lender and ask about your home loan application status by providing your application ID/ reference number.

Only mentioned relatives are eligible to be co-applicants for home finance:

Unmarried Sons and daughters can apply for a joint home loan with their parents. A husband and wife can apply jointly. A brother and a sister can apply for a home loan together, but a brother-sister or sister-sister pairing is not permitted.

Bajaj Finserv Home Loan

Overview

With a home loan from Bajaj Finance you can achieve your homeownership goal effortlessly. Depending on your eligibility, you can access a home loan of up to Rs. 15 Crore*. We provide competitive interest rates for both salaried and self-employed individuals. With EMIs as affordable as Rs. 664/lakh* and a flexible repayment period extending up to 32 years*, you can manage repayment at your convenience. Our hassle-free online application process ensures disbursal within just 48 Hours*. Additionally, benefit from our home loan balance transfer option, offering an added top-up for managing additional expenses.

Features and Benefits of our Home Loan

- Loan of up to Rs. 15 Crore*: Purchasing a home marks a significant milestone. Achieve it with the substantial amount of up to Rs. 15 Crore* available through Bajaj Finserv Home Loan.

- Competitive interest rates: Start with our loan interest rates as low as 7.15%* p.a, allowing you to pay EMIs as minimal as Rs. 664/lakh*.

- Approval in 48 Hours*: Your loan application will be approved within 48 Hours* of your application, in some cases, even earlier.

- Tenure of up to 32 years: Repay your loan comfortably with our extended repayment tenure of up to 32 years.

- No foreclosure fee for individuals: Individual borrowers opting for a floating interest rate can foreclose the entire amount or prepay a part of the loan without incurring any additional fees.

- Hassle-free application: Skip numerous branch visits with our doorstep document pick-up service, ensuring a hassle-free application process.

- Balance Transfer facility: Benefit from our home loan balance transfer facility and be eligible for a top-up loan of up to Rs. 1 crore* or higher.